Office Loan Distress Hit a Record in 2026 — What It Means for Owners

Office delinquencies just set an all-time high, and lenders are ending the “extend and pretend” era. Here’s what’s driving it — and what commercial owners in Kentuckiana should know.

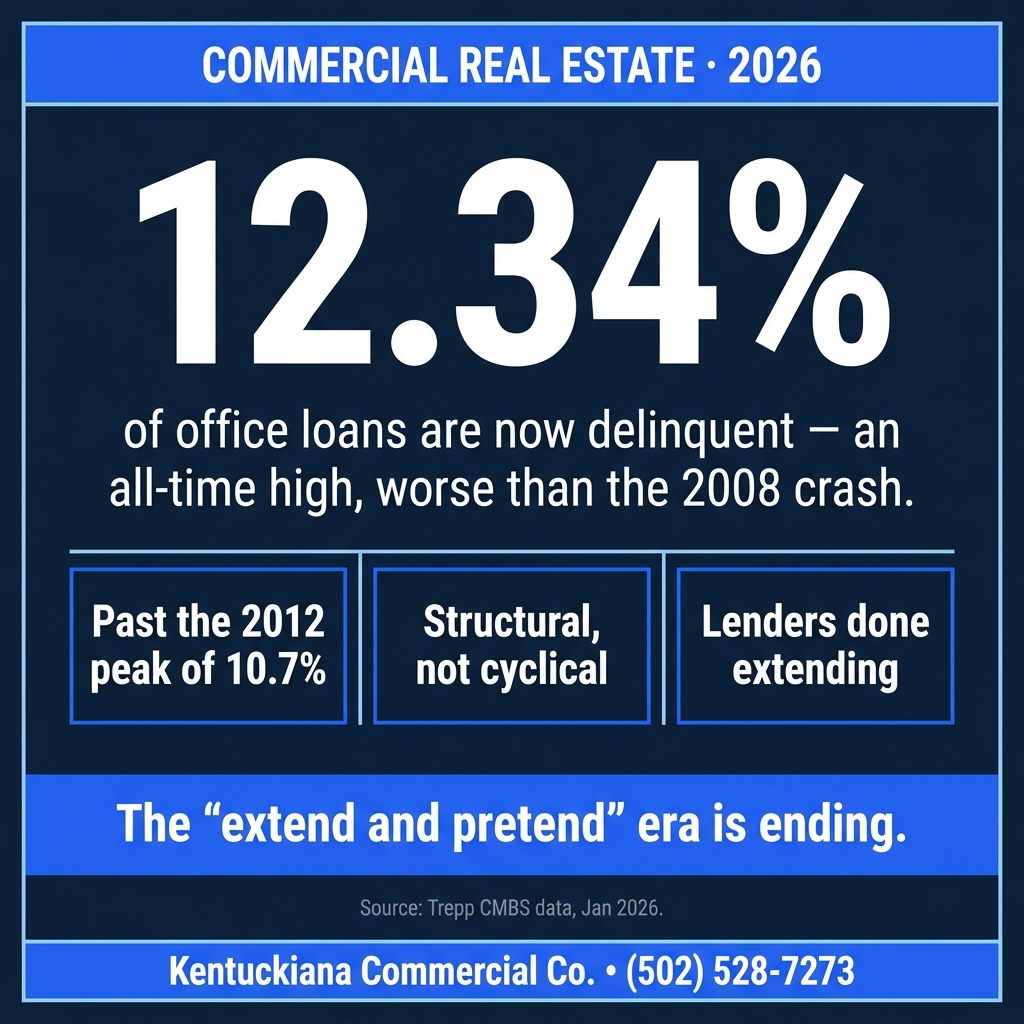

The headline number

In January 2026, the delinquency rate on office loans bundled into commercial mortgage-backed securities (CMBS) reached 12.34% — an all-time high, and the worst reading since this data has been tracked (back to 2000). It surpassed the previous cycle peak of roughly 10.7%, set in late 2012 in the aftermath of the global financial crisis. In plain terms: a larger share of office loans is behind or in trouble today than at any point in the modern record, including the last crash.

Why this cycle is different

The analysts at Trepp characterize today’s office stress as structural, not cyclical. It isn’t that offices suddenly stopped collecting rent; it’s a collision of three forces: interest rates that roughly doubled from the 3–4% era, weaker leasing demand, and a lasting shift in how much office space companies actually use after the move to hybrid and remote work. The distress is being driven primarily by refinancing pressure rather than a wholesale collapse in operations — which is exactly why it lands hardest as loans come due.

The end of “extend and pretend”

For the past few years, many lenders played “extend and pretend” — rolling maturing loans forward and hoping rates would fall and values would recover. That patience is wearing thin. Where extensions do still happen, they buy time rather than solve the problem: in February 2026, the overall CMBS delinquency rate actually dipped as lenders modified and extended a handful of large office and mall loans, with office extensions ranging from about one month to nearly three years. The underlying math doesn’t change — it just moves the deadline.

It’s not only an office problem

The sharpest distress is concentrated in older, “commodity” office buildings. But the force underneath it — loans written cheap now resetting expensive — touches every commercial asset class as maturities arrive: retail, industrial, multifamily, mixed-use. Office is simply the leading edge of a broader repricing.

What it means if you own commercial property

If you own a commercial building and your loan is maturing into a market where the bank won’t extend and won’t refinance on workable terms, your options narrow to a familiar few: bring additional cash to close a refinance, restructure with the lender, or sell. The owners who keep the most control are the ones who look at those options early — before a special servicer or a foreclosure calendar makes the decision for them.

How a direct sale fits

Selling to a direct buyer is one of those options, and for some owners it’s the cleanest one. Kentuckiana Commercial Co. buys commercial property across Southern Indiana and the Louisville metro for cash, as-is, on a certain closing date — no financing contingency to fall through, no lender approval to wait on. For an owner staring at a maturity date they can’t refinance past, that certainty can be worth more than squeezing for the last dollar in a stalled market.

Questions owners are asking

What is the office CMBS delinquency rate in 2026?

Office loan delinquencies reached 12.34% in January 2026 — an all-time high that surpassed the roughly 10.7% peak reached after the 2008 financial crisis.

Is the office distress cyclical or structural?

Analysts at Trepp describe it as structural rather than cyclical — driven by higher interest rates, weaker leasing demand, and lasting shifts in how offices are used.

My loan is maturing and the bank won’t extend. What are my options?

Owners generally choose among refinancing (if the numbers work), injecting additional equity, restructuring with the lender, or selling. A direct cash sale offers a certain closing date without a financing contingency.

Where owners go from here

Loan maturing and the math doesn’t work?

Tell us about the building and the timeline. We can offer a certain, cash closing date — free, confidential, and no obligation.