The 2026 Commercial Mortgage Maturity Wall — and the Refinancing Gap

About $930 billion in commercial mortgages come due in 2026, much of it financed when rates were half what they are today. Here’s what the “maturity wall” means for owners — and the number underneath it that actually decides outcomes.

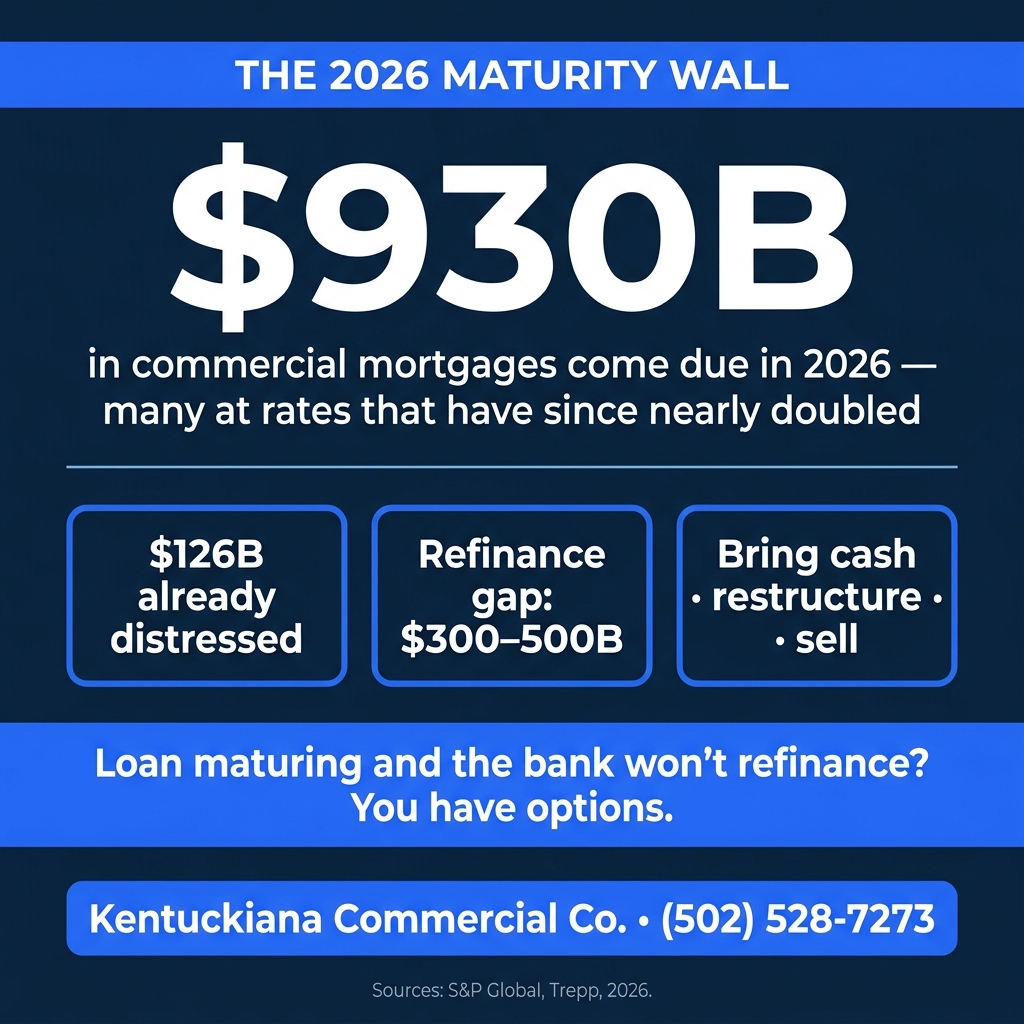

How big is the wall?

Roughly $930 billion in commercial mortgages mature in 2026, and at least $126 billion of that was already considered distressed heading into the year. Zoom out and it’s larger still: cumulatively, well over $1.5 trillion of commercial real estate debt will have reached maturity by year-end. S&P Global expects the broader “maturity wall” to peak at about $1.26 trillion in 2027, up from roughly $950 billion in 2024. This is one of the largest refinancing waves the industry has faced.

Why it’s hitting now

Most of this debt was written in the 2010s, on five- to ten-year terms, at rates of 3–4%. Those loans are coming due in a short span and colliding with a very different world — refinance rates that are often nearly double, plus more conservative underwriting. A loan that made easy sense a decade ago doesn’t automatically pencil today.

The refinancing gap: the number that matters

The headline maturity figure gets the attention, but the refinancing gap is the actionable number. With higher rates and tighter underwriting, a new loan covers a smaller share of value than the old one did. The gap — the owner’s existing balance minus the proceeds a new loan will actually provide — is the equity the owner must bring just to keep the property. Multiply that across thousands of buildings and the market-wide gap is estimated at $300–500 billion. When the gap is too large to fill, the options narrow.

What it looks like on a single building

Consider a 2014-vintage loan originated at a 4.5% coupon on an interest-only structure. Sized to today’s constraints — a ~6.5% coupon, conservative debt-service coverage, and a lower loan-to-value ceiling — a new loan might cover only around 65% of the existing balance. The remaining ~35% is cash the sponsor has to produce, or the trigger for a workout or sale.

Three doors

When refinancing alone won’t bridge the gap, owners generally face three doors: bring the cash, restructure with the lender, or sell. There’s no universally right answer — it depends on the building, the equity, and the timeline. What hurts owners most is waiting until the maturity date is on top of them and the doors have narrowed to one.

Where a direct sale fits

If the refinance math doesn’t work and you’d rather choose your own outcome than have a lender choose it for you, selling is a legitimate door — and often the fastest. Kentuckiana Commercial Co. buys commercial property across Southern Indiana and the Louisville metro for cash, as-is, on a certain closing date — no financing contingency, no waiting on an approval that may not come. Selling on your own terms beats defaulting on the bank’s.

Questions owners are asking

How much commercial real estate debt matures in 2026?

Roughly $930 billion in commercial mortgages mature in 2026, with at least $126 billion already considered distressed. Cumulatively, well over $1.5 trillion will have reached maturity by year-end.

What is the refinancing gap?

The shortfall between an owner’s existing loan balance and what a new loan will cover at today’s higher rates — estimated at $300–500 billion market-wide. It’s the equity owners must bring, or the trigger for a sale or workout.

What if I can’t refinance my maturing loan?

Owners generally choose among bringing additional equity, restructuring with the lender, or selling. A direct cash sale offers a certain closing date without a financing contingency.

Where owners go from here

Staring down a maturity date?

Tell us about the building and the timeline. We can offer a certain, cash closing date before the wall hits — free, confidential, no obligation.